The Practice of ESG Report Standards

——Take the group standard "Guidance on drafting environmental, social and corporate governance (ESG) reports for information and communication enterprises " as an example

Abstract: Information disclosure and ESG report preparation are the essential work of corporate ESG governance. They are the key for stakeholders to obtain complete, timely, accurate, measurable, and comparable corporate ESG information. They are also the key for rating agencies to carry out ESG ratings and investment institutions to start ESG. The first step in investing, therefore, is that ESG information disclosure is crucial to ESG governance. To further standardize the ESG information disclosure and report preparation of electronic information companies, based on the global ESG reporting guidelines or standards, based on the characteristics of the electronic information industry and the demands of stakeholders, and combined with the ESG report disclosure practices of listed companies, the China Electronics Chamber of Commerce initiated a project to formulate The group standard "Guidance on drafting environmental, social and corporate governance (ESG) reports for information and communication enterprises" summarizes the principles for the preparation of ESG reports and clarifies the material topics and content of ESG disclosure by electronic information enterprises, to strengthen the ESG capacity building of enterprises and assist electronic information enterprises: sustainable development and high-quality development of the information industry.

Keywords: information disclosure, ESG reporting, electronic information companies, group standards

I. INTRODUCTION

With the continuous and in-depth development of environmental, social, and corporate governance concepts, ESG has gradually become a new navigation beacon for outstanding companies and a new yardstick for risk assessment and value measurement of investment institutions. In order to better meet the demands of stakeholders and continuously improve the sustainable development and influence of enterprises, more and more enterprises (especially listed companies) have begun to disclose ESG information and standardize their own ESG management.

From the practical point of view of Chinese and foreign enterprises, ESG information disclosure provides stakeholders with environmental, social, and governance performance data, enhances the transparency of enterprises, reduces the uncertainty of enterprise development, which helps to establish trust relationships with users, helps to develop a solid partnership with investors, is conducive to attracting long-term investment; At the same time, ESG information disclosure allows enterprises to pay attention to, identify, assess and manage potential environmental, social and governance risks to develop appropriate risk management strategies in advance and reduce potential losses in the development process. Moreover, along with the United Nations concept of "sustainable development goals" and "responsible investment" and the Chinese government's development strategy of "Common Prosperity" and "Chinese-style modernization", ESG governance is conducive to high-quality development of enterprises, especially central enterprises, state-owned enterprises, and leading enterprises.

Through tracking and research on various forms of ESG information disclosure by listed companies, including ESG reports, company annual reports, etc., we have found that there are five common problems in ESG information disclosure by domestic companies:

First, there needs to be more awareness of ESG. From the top decision-making level of the company to the employee level, it is generally believed that ESG increases corporate costs and is forced to disclose ESG information (reports). Second, the disclosure objective needs to be clarified, and the leading company has many affiliated companies. There is a great deal of arbitrariness in which one is used as the subject of information disclosure; third, the content of the disclosure could be more precise, more standard, and more arbitrary. There is "selective disclosure and selective non-disclosure." Specifically, it is easy for enterprises to disclose information. Companies will vigorously disclose those things that have been done and have achieved specific results. Still, companies will selectively ignore those that are not easy for companies to do in a short time or the results are not very obvious, resulting in domestic ESG reports that are "one size fits all" , has even become the company's annual work summary or the company's "publicity materials + product manuals." Fourth, data quality needs to be improved; there is more qualitative data than quantitative data, and the comparability of the data could be better, which is not conducive to accurate comparison and ESG rating. Fifth, ESG information disclosure (reporting) needs more professional work teams, standard operating procedures (SOPs), and necessary technical tools. Many companies form temporary groups or outsource, lacking unified management and long-term consistency.

Therefore, the ESG information disclosure framework that meets international standards, meets ESG management and investment needs, and combines industry characteristics and stakeholder demands has attracted the attention of industry enterprises. For this purpose, the China Electronics Chamber of Commerce (CECC)initiated a project to formulate The group standard "Guidance on drafting environmental, social and corporate governance (ESG) reports for information and communication enterprises" ( referred to as "group standard").

Ⅱ. Research on existing standards or rules

In terms of ESG information disclosure, many international organizations around the world have issued relevant disclosure standards, the most important of which include the Sustainable Development Goals (SDGs) promoted by the United Nations and the Task Force on Climate-related Financial Disclosure (Task Force on Climate -- The "Recommendations Report of the Working Group on Climate-related Financial Disclosures" issued by TCFD), the sustainable accounting standards issued by the Sustainability Accounting Standards Board (SASB), the International Global Reporting Initiative (Global Reporting Initiative, GRI's "Sustainability Report Preparation Guidelines" and the International Sustainability Standards Board (ISSB)'s sustainable disclosure standards IFRS S1 and IFRS S2 have put forward new requirements for ESG information compliance disclosure.

The United Nations Sustainable Development Goals (SDGs, 2015) are related to the global consensus on global sustainable development and are the responsibilities of every corporate citizen. They are also the ultimate goal of ESG governance and should be the core element of ESG information disclosure. It is indeed the case in practice. The environment, society, and corporate governance the ESG concept focuses on all correspond to the United Nations Sustainable Development Goals (Table 1). Almost every mainstream ESG information disclosure has corresponded with the SDGs.

Table 1 The corresponding association between ESG and SDGs

TCFD is currently the most influential and widely supported climate information disclosure standard in the world. It not only promotes institutional consistency among G20 member states but also provides a common framework for the disclosure of climate-related financial information. The TCFD framework was launched in 2017, including four major sections: governance, strategy, risk management, metrics and targets.

In November 2018, SASB released a set of globally applicable specific standards for 77 industries, including six levels: general disclosure guidance, industry description, sustainability topics and descriptions, sustainability accounting standards, technical protocols, and activity metrics.

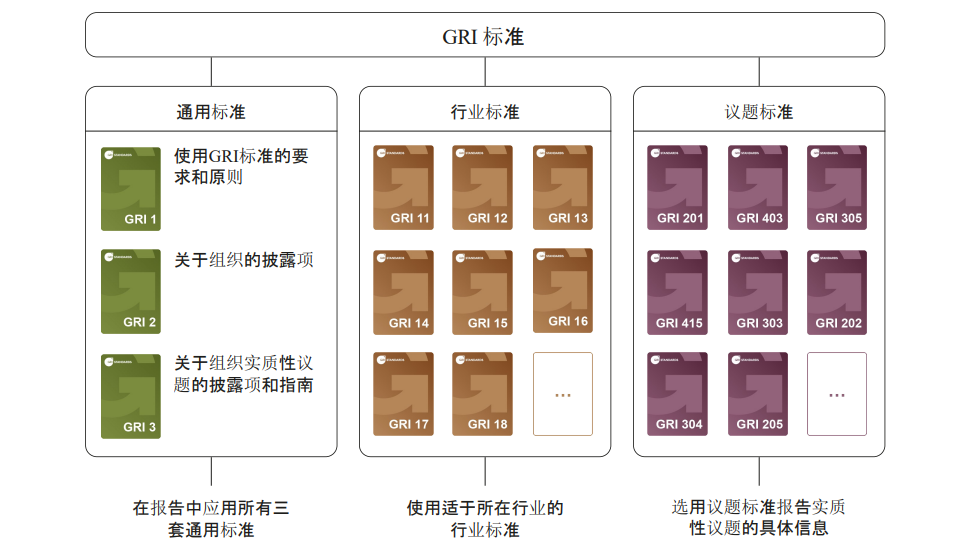

GRI released the world's first sustainability reporting guidelines in 2000. The latest GRI2021 standards take effect on January 1, 2023. They are composed of multiple sets of interrelated standards, divided into general standards, industry standards, and issue standards. The general standards include GRI 1, GRI 2 and GRI 3. GRI 1 explains the purpose and system of the GRI standard, explains the fundamental concepts of sustainability reporting, and explains the nine requirements and eight reporting principles that organizations must comply with to comply with the GRI standards preparation report. GRI 2 introduces 30 disclosures for organizations to describe reporting practices and other organizational details (such as activities, governance, and policies) to describe the organization's profile and size and provide context for understanding the organization's impact. GRI 3 provides step-by-step guidance on how to identify material issues, as well as a series of disclosure items for organizations to describe their process for identifying material issues, a list of the material problems, and how each case is managed.

By integrating the resources of TCFD and SASB, ISSB released IFRS S1 and IFRS S2 in June 2023. It drew on TCFD (governance, strategy, risk management, metrics and targets) in terms of core content and integrated SASB into relevant disclosure requirements. CDSB and IIRC-related content partially refer to GRI standards. In October 2021, G20 leaders held the Rome Summit and issued a communiqué clearly supporting the ISSB as an international sustainability standard-setting organization. In September 2023, they reissued a communiqué welcoming the ISSB's release of two sustainable disclosure standards.

Compared with the international standards, although there is no unified ESG information disclosure framework and ESG report compilation basis in China at present, regulators and relevant government departments have incorporated ESG into relevant information disclosure guidance documents, mainly including Shenzhen Stock Exchange's guidance on social responsibility of listed companies in Shenzhen Stock Exchange in 2006 and Shanghai stock exchange's guidance on environmental information disclosure of listed companies in Shanghai Stock Exchange in 2008. The "Environmental, Social and Governance Report Guidelines" (revised version) issued by the Hong Kong Exchange in 2019, and the "Work Plan for Improving the Quality of Listed Companies Controlled by Central Enterprises" published by the State Council SASAC in 2022, etc.

At the same time, domestic industry organizations are concerned about the preparation of ESG reports, such as the China Enterprise Reform and Development Research Association released the "Enterprise ESG Report Compilation Guide" (T/CERDS 4-2022), the "Enterprise ESG Disclosure Guide" (T/CERDS 2-2022), among which the "China Corporate Social Responsibility Report Guidelines (CASS-CSR4.0) and (CASS-ESG5.0)" by the Social Responsibility Research Center of the Ministry of Economics of the Chinese Academy of Social Sciences.

III. Process of Standard Formulation

In March 2023, the China Electronic Chamber of Commerce officially established the workgroup of "group standard", whose members include ZCX Green Gold Technology (Beijing) Co., Ltd., Institute of Enterprise Data and Analytics (Beijing) Co., Ltd, and Lenovo (Beijing) Co., Ltd., etc. The working group proposed a plan for the preparation of this standard by reviewing relevant information, standards, and research, combined with the current status of ESG report preparation by electronic information companies and existing questions in ESG information disclosure.

From March 14 to April 6, 2023, the working group formed a standard drafting group, held a project kick-off meeting, and clarified the work progress, task division, research plan, and other arrangements for standard preparation;

From April 7 to July 12, 2023, the working group conducted a large amount of research and investigation work, successively reviewed relevant literature and collected information related to ESG of electronic information companies, and formed "group standard", The first draft of the "Report Preparation Guidelines," after many discussions, formed the "Draft for Comments" and "Preparation Instructions." Based on the "Draft for Comments," opinions and suggestions from institutions or enterprises were extensively collected. A total of 95 revision opinions or recommendations were received, of which 39 were fully adopted, 22 were partially adopted, and 34 were not adopted.

On August 24, 2023, the working group held a group standard review meeting for "group standard", Based on the principles of scientific truth-seeking and coordination, the working group reviewed all aspects of the standard draft for review. The content is entirely, carefully, and meticulously discussed and reviewed.

In September 2023, the working group conducted multiple communications with experts revised and improved the content of the draft for review based on the opinions put forward by the expert review team. Finally, it formed a draft for approval on this basis.

On September 20, 2023, the China Electronics Chamber of Commerce announced "group standard", numbered T/CECC 022-2023, which will be implemented from the date of announcement, and the National Group Standards Information Platform of the China Institute of Standardization released "group standard".

IV. Basic issues of information disclosure

Referring to the basic idea of the GRI standard, a complete ESG information disclosure (report compilation) standard should clearly tell the enterprises preparing to disclose ESG information a series of basic and key processes and methods, including whether the standard is applicable to their own organizations (Organization)? How do they identify stakeholders (Stakeholder)? How to identify material topics (Material Topics)? How do they organize a team to collect, sort out, and publish information (SOP)? How to respond to information disclosure for improvement (Responsibility)? This is a complete ESG information disclosure closed loop, and the workgroup will conduct in-depth research and discussion on these basic issues.

ⅰ. Applicable enterprise scope

Enterprises related to the manufacturing and service of electronic information and household electrical appliances, including "C 39 computer, communication, and other electronic equipment manufacturing industry", "I 63 telecommunication, radio and television, and satellite transmission services", "I 64 Internet and related services", "I 65 software and information technology service industry" and "C 385 household electrical appliance manufacturing" in "National economic industry classification GB/T4754-2017", including major electronic information industry enterprises.

Only after the enterprise has been determined can the enterprise's stakeholders and material topics be determined based on the characteristics of the industry and enterprise.

ⅱ. Terms and definitions

In accordance with the requirements for standard preparation, several types of terms and their definitions involved in the standard are listed, and their connotations and denotations are clarified in order to achieve comparability of information content, including:

The first category is basic ESG terms: ESG reporting, stakeholders, material issues, greenhouse gases, risk management, investors, data security, sensitive personal information, and sustainable development.

The second type of industry characteristic terms: electronic information enterprises, electronic information product pollution, toxic and harmful substances or elements, green data centers, remanufactured products, extended producer responsibility system, critical information infrastructure, network security, virtual communities, "three simultaneous" terms such as system and data center power usage efficiency.

ⅲ. Principles

The principles for preparing ESG reports for electronic information companies are defined, involving ten principles, including materiality, accuracy, authenticity, quantification, completeness, objectivity, consistency, continuity, timeliness, and readability.

ⅳ Report compilation and disclosure process

Standardizes the preparation and disclosure process of ESG reports for electronic information companies, including the establishment of a particular working group to regularly and collect entirely, sort out, and calculate relevant data and information during the reporting period, and carry out report preparation, layout, disclosure or release and review summary Waiting for the process arrangement.

ⅴ. Identification of stakeholders

By analyzing the characteristics of the electronic information industry and corporate operating characteristics, identify and determine internal and external stakeholders, including but not limited to the following categories:

a) Customers or consumers: including businesses (2B) and individuals (2C), such as customers of software and electronic product companies.

b) Government departments and regulatory agencies, including industry and information technology, network supervision, environmental protection, finance, etc.

c) Investors: including strategic investors, secondary market investors, etc.

d) Senior management personnel of the enterprise: including shareholders’ meeting, board of directors, board of supervisors, operating management, etc.;

e) Company employees;

f) Suppliers or partners;

g) Community;

h) Media, etc., including the increasingly influential self-media, etc.

ⅵ. Identification of material topics with characteristics of the electronic information industry

First of all, in terms of the environment, the rapid development of the electronic information industry has accelerated the update and iteration of electronic information technology and products, and the amount of electronic product waste generated subsequently has also increased year by year. In addition, as the fifth largest energy-consuming industry in the world, the energy consumption of data centers has also attracted many concerns. In June 2022, the Ministry of Industry and Information Technology, the National Development and Reform Commission, the Ministry of Ecological Environment, and six other departments jointly issued the "Industrial Energy Efficiency Improvement Action Plan" to promote the green upgrading of energy efficiency in key areas, including continuing to carry out the construction of national green data centers, guiding data centers to expand the proportion of green energy utilization, and promoting the implementation of system energy conservation transformation in old data centers.

Therefore, based on the above characteristics of the electronic information industry, the proposed environmental dimension material topics include waste management (E.3), energy consumption level and management measures (E.4), energy efficiency level of data centers (E.6), coping with climate change (E.2) and other topics.

Secondly, in the social aspect, in the fierce market competition environment, the performance of product quality management and technical personnel reserve is significant for electronic information enterprises, especially in the quality control of upstream supply materials and the implementation of quality control in the manufacturing process, which plays a vital role in improving product competitiveness and market reputation; At the same time, data security, as an essential guarantee for the development of electronic information enterprises, has been paid attention and valued by the state, especially with the institutional reform of the State Council, data security will be upgraded to a new height.

Based on the above characteristics, the material topics of the social dimension are formulated, including product quality and customer service (S.1), supplier management (S.7), employee responsibility (S.5), data security and network security management (S.2) and other topic content.

Third, in terms of corporate governance, as a technology-intensive industry, technology and R&D capabilities are one of the core competitive elements of enterprises in the industry. However, the current electronic information industry is currently suffering from technical barriers, and some machinery and equipment, raw materials, and parts are still dependent on imports. It is urgent to achieve technological breakthroughs to get rid of the dependence on upstream suppliers and achieve sustainable development. At the same time, the electronic information industry is facing rapid demand changes, and the research and development capabilities of enterprises, product advancement, and internal efficient governance have also been put to the test.

Based on the above characteristics, the material topics of the corporate governance dimension are proposed, including R&D innovation investment and intellectual property protection (G.5), compliance risk management (G.3), and other topics.

V. Basic framework of ESG report for electronic information enterprises

Slightly different from the GRI and CASS framework systems, "group standard" combines the above applicable enterprise and scope, terms and definitions, principles, Report compilation and disclosure process, and identification of stakeholders, as the basic common sense of ESG information disclosure (reporting), does not focus on them, but focuses on refining material topics with the characteristics of the electronic information industry, similar to GRI's industry standards (GRI11/12/13), which is considered based on the most questions raised by enterprises in practice.

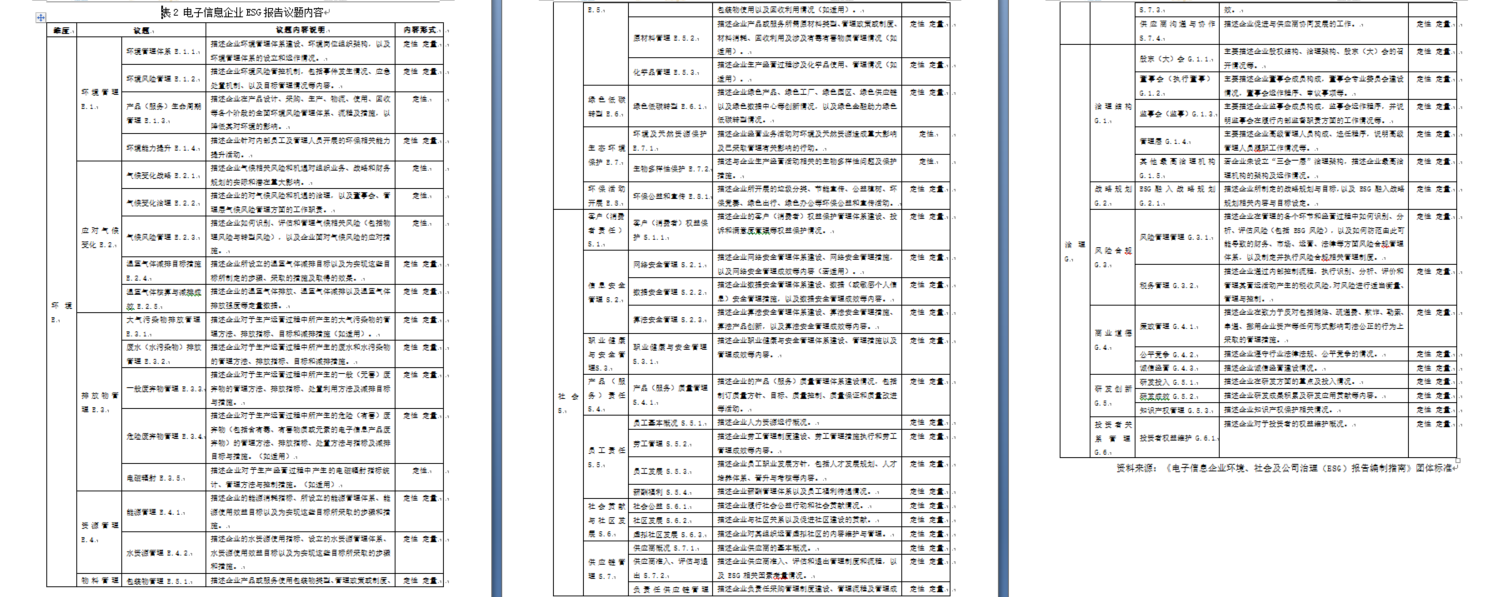

ⅰ. The content of the material topics

Table 2 ESG report topics of electronic information enterprises

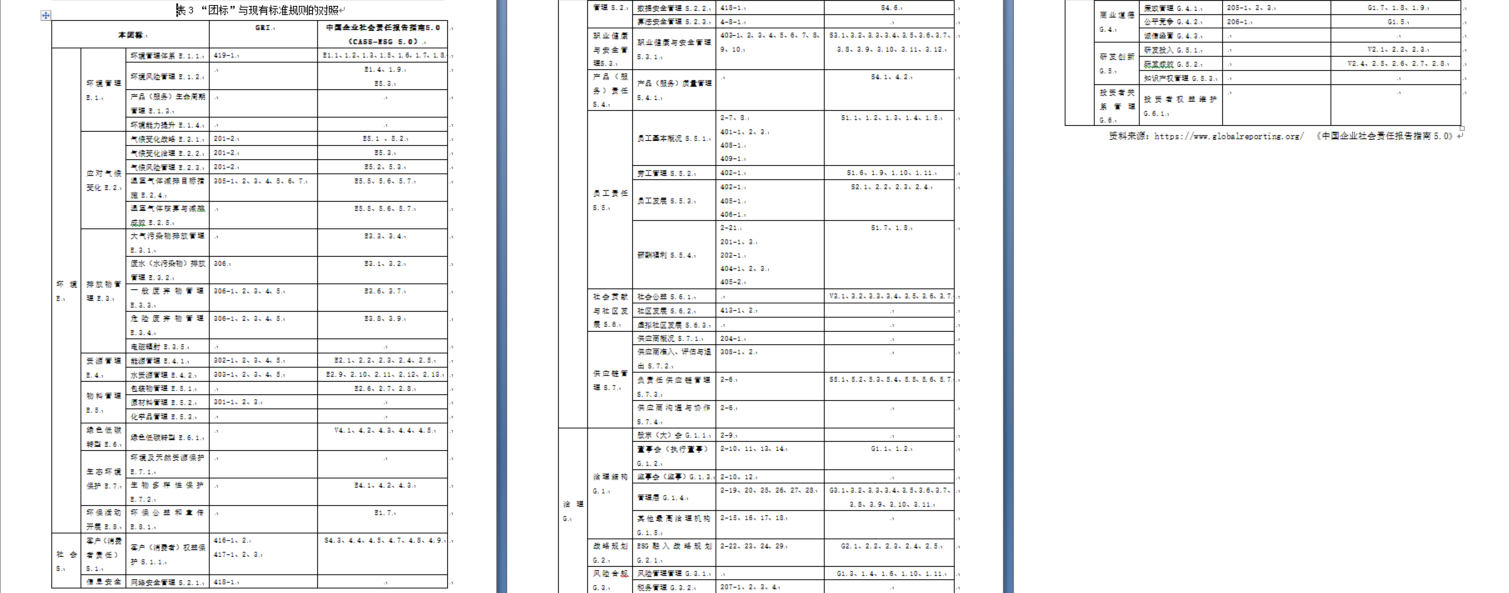

ⅱ. Comparison with existing standards and guidelines

Table 3 comparison between this regiment and existing standards and guidelines

ⅲ. the main features and shortcomings of the guidance

In short, "group standard" mainly has the following five characteristics: Firstly, fully absorb and draw on the experience of existing international and domestic information disclosure standards and rules, reduce the discomfort of enterprises towards the variety of standards, and enhance the comparability of rules. Secondly, reflecting Chinese characteristics, especially in terms of the framework of rules, the system of international standards is relatively complete, generally starting from a micro perspective. This group aims to establish a meso perspective, which is convenient for domestic enterprises to establish a systematic concept and enforceability of ESG information disclosure. Thirdly, highlight the characteristics of the electronic information industry, especially those related to information security, privacy protection, responsible supply chain management, and electronic waste management. Fourthly, seek truth from facts and fully consider the current reality of ESG governance in electronic information enterprises in order to encourage enterprises to "do more than do well" in ESG information disclosure. Fifth, the qualitative content disclosed still accounts for the main proportion, which is not conducive to quantitative analysis and needs to be continuously improved and developed in the future.

VI. Conclusion

The group standard "Guidance on drafting environmental, social and corporate governance (ESG) reports for information and communication enterprise" is a valuable practice for ESG information disclosure by the China Electronics Chamber of Commerce as a third-party organization. It responds to the high-quality needs of enterprises and brings together the ESG industry and electronic information—expert wisdom in the industry and drawing on international experience. Although not perfect and comprehensive, it has taken the first step. We look forward to the standardized disclosure of ESG information for electronic information companies and the extensive promotion and sustainable promotion of ESG investment in the electronic information industry. The development concept takes root in the enterprise and contributes its professional strength to Chinese-style modernization.

The Group Standards Technical Review Committee of the China Electronics Chamber of Commerce heard the explanation of the standard preparation process, standard content, and other related issues by the group standards working group and considered that the documents were complete, standardized, and in compliance with relevant requirements. "group standard" clarifies the ESG disclosure material topics and content, and work processes of enterprises in the electronic information industry, provides ESG information disclosure reference for enterprises in the electronic information industry, and will promote the improvement of ESG disclosure levels of enterprises in the electronic information industry, thereby promoting the electronic information industry. The standardized development of ESG management for enterprises in the information industry is normative, scientific, feasible, and rational and complies with the requirements of current relevant national laws and regulations.

"Group standard" is effective after September 20, 2023. We will closely follow the feedback from enterprises in the application, continuously revise and improve it, set the standard for the future industry standards, and even complete the essential work to construct national standards.

VII. References

[1] United Nations Sustainable Development Goals, https://sdgs.un.org/goals

[2] Task Force on Climate-Related Financial Disclosures, https://www.fsb-tcfd.org/

[3] Sustainability Accounting Standards Board, https://sasb.org/

[4] International Sustainability Standards Board, https://www.ifrs.org/groups/international-sustainability-standards-board/

[5] Global Reporting Initiative, https://www.globalreporting.org/

[6] China Securities Regulatory Commission "governance guidelines for listed companies", 2018

[7] Environment, society and governance report guidelines of the Stock Exchange of Hong Kong Limited

[8] Corporate Governance Code of the Stock Exchange of Hong Kong Limited

[9] Shanghai Stock Exchange "guidelines on environmental information disclosure of listed companies"

[10] Shenzhen Stock Exchange "guidelines on social responsibility of listed enterprises"

[11] China Electronics Industry Standardization Technology Association "electronic information industry social responsibility governance evaluation index system" T/CESA 16003-2021

[12] Social Responsibility Research Center of economics department of Chinese Academy of Social Sciences "China Enterprise Social Responsibility Report guide 5.0"

后记按:英文版由陈伟祺翻译和编辑。作者完成联合国可持续发展ESG高级研修班的全部课程学习,通过了论文审核,特颁ESG高级策略顾问培训证书。

联合国训练研究所(United Nations Institute for Training and Research,UNitar)成立于一九六三年,总部位于瑞士日内瓦,是联合国大会直属最高级别事务执行机构,主要承担联合国系统中的培训和研究两项职能。

联合国训练研究所全球培训网络目前由三十个国际培训中心组成,遍布亚洲,非洲,澳大利亚,欧洲,美洲和加勒比地区,在全世界范围内提供创新培训,是政府部门,私营企业和社会中介性组织之间交流知识的枢纽。